AI in banking and insurance is swiftly changing, as well as other industries in the world. By automating everyday tasks and delivering personalized customer experiences, AI is fundamentally altering the operations of these institutions and their interactions with clients. This blog post delves into the developing role of AI in banking and insurance, highlighting its current uses, potential advantages, and the challenges that may arise in the future.

>> Read more: The Future of AI Fraud Detection and Prevention in BFSI

1. Current applications of AI in banking and insurance

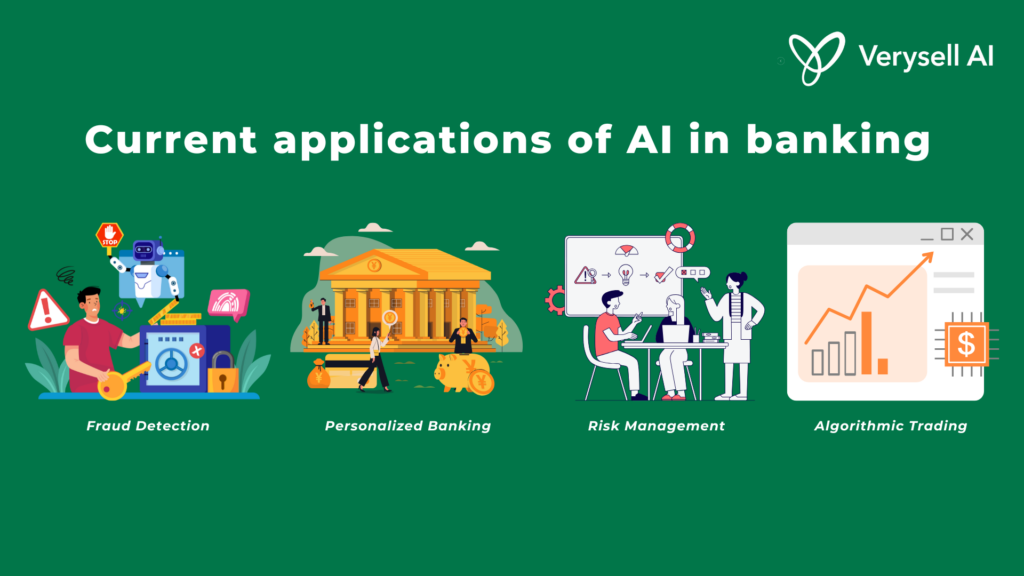

1.1 Current applications of AI in banking

The banking sector is utilizing AI in numerous ways to boost efficiency, security, and customer satisfaction. Key applications include:

Fraud detection: AI algorithms analyze large volumes of transaction data to detect suspicious patterns and prevent fraud in real-time. Fraud detection is significantly more effective than traditional rule-based systems, which often lag the evolving tactics of fraudsters. AI can learn and adapt, identifying subtle irregularities that may otherwise go unnoticed.

Personalized Banking: AI-driven chatbots and virtual assistants are becoming more prevalent, providing 24/7 support and tailored financial advice to customers. These systems can handle inquiries, process transactions, and suggest personalized product recommendations based on individual financial profiles. This enhances customer service while allowing human advisors to concentrate on more complex matters.

Risk Management: AI algorithms evaluate creditworthiness and forecast loan defaults more accurately than traditional approaches to manage risks. By analyzing a broader range of data points, including alternative credit information, AI offers a more comprehensive view of a person’s financial status, leading to better-informed lending decisions.

Algorithmic Trading: AI is widely used in algorithmic trading, where sophisticated algorithms execute trades rapidly based on predetermined parameters. This enables financial institutions to take advantage of market fluctuations and refine their trading strategies.

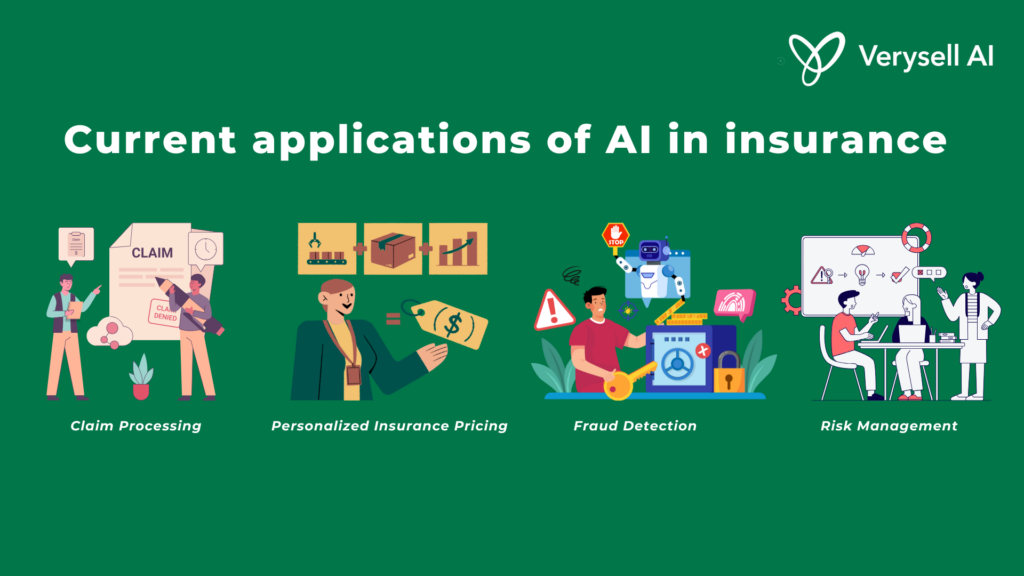

1.2 Current applications of AI in insurance

The insurance industry is increasingly adopting AI to enhance efficiency, personalize services, and manage risk more effectively. Key applications include:

Claims Processing: AI can streamline the claims process by analyzing documents, images, and other data to evaluate claim validity and accelerate payouts. This leads to reduced processing times and heightened customer satisfaction.

Personalized Insurance Pricing: AI-powered virtual assistants analyze extensive data, such as driving records, health histories, and lifestyle factors, to determine personalized insurance premiums via AI-driven chatbots and virtual assistants. This enables insurers to offer more competitive rates to enhance customer experience while effectively managing risk.

Fraud Detection: Like in banking, AI can identify fraudulent insurance claims by detecting suspicious patterns and inconsistencies in the data. This helps insurers reduce losses and maintain affordable premiums.

Risk Assessment: AI enhances risk evaluation by analyzing data from diverse sources, including weather patterns, traffic information, and even social media activities. This comprehensive analysis allows insurers to better understand and manage their exposure to various risks.

2. Benefits of AI in banking and insurance

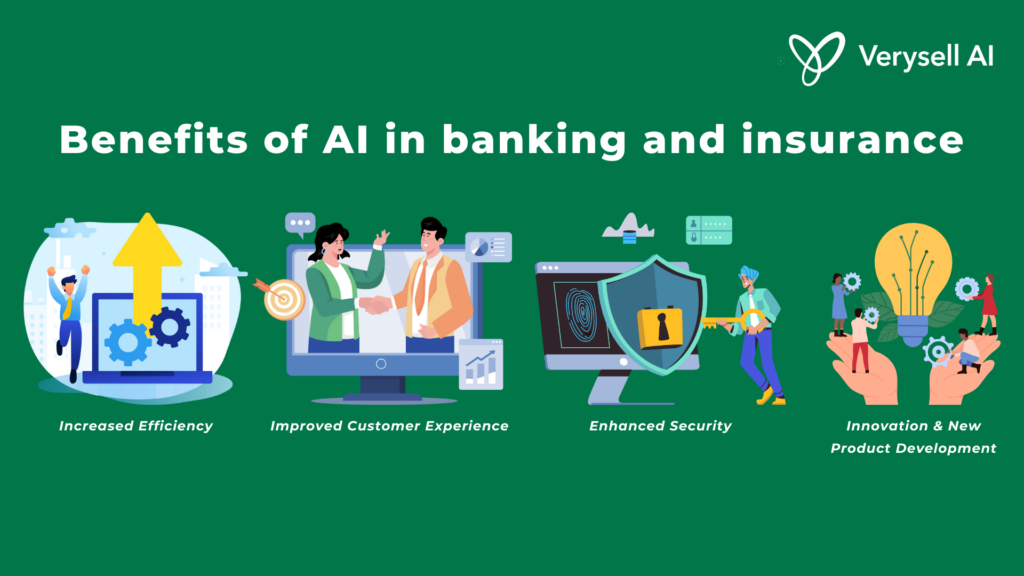

The widespread implementation of AI in banking and insurance presents several potential advantages, including:

Increased Efficiency: AI can automate routine tasks, allowing human employees to concentrate on more complex and strategic initiatives. This results in higher productivity and lower operational costs. Moreover, by freeing up valuable time and resources, AI enables employees to engage in creative problem-solving and innovation, driving overall business growth. This shift not only enhances job satisfaction but also fosters a more agile and responsive organizational culture.

Improved Customer Experience: Same the retail industry, AI-driven chatbots and personalized services enhance customer satisfaction by offering immediate assistance and customized solutions. With the usage of AI, retailers can gather valuable insights into consumer behavior, helping them refine their strategies and enhance engagement.

Enhanced Security: AI algorithms are more effective at detecting and preventing fraud compared to traditional methods, safeguarding both customers and financial institutions from financial crimes.

Innovation and New Product Development: AI can facilitate the creation of innovative products and services that cater to the changing needs of customers. This agility in product development not only meets current demands but also anticipates future needs, positioning companies as leaders in their respective markets.

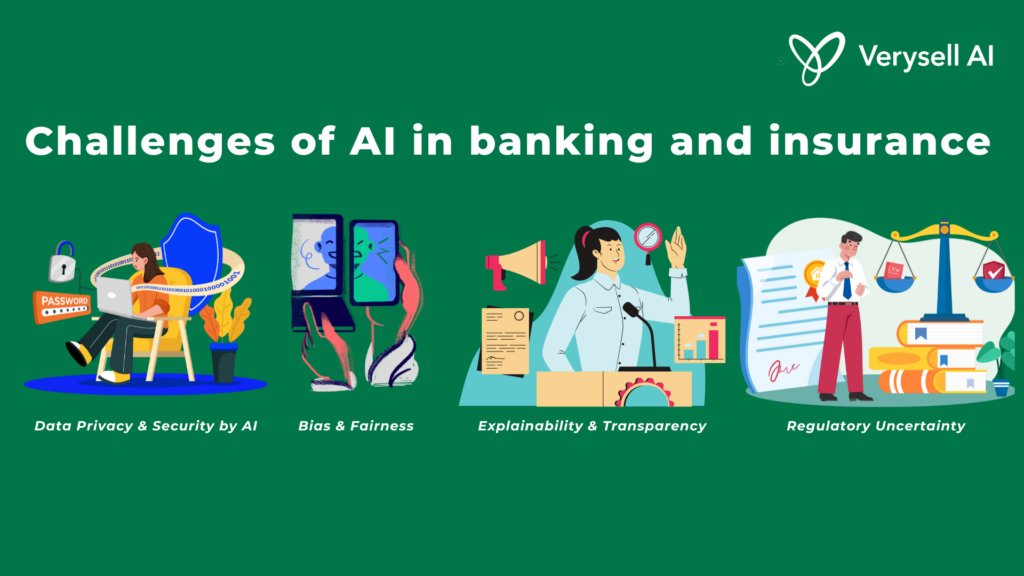

3. Challenges of AI in banking and insurance

While there are many advantages to adopting AI in banking and insurance, several challenges also arise:

Data Privacy and Security: AI algorithms depend on large amounts of data, which raises concerns about privacy and security. Financial institutions must ensure responsible data collection and usage in compliance with applicable regulations. By fostering a culture of transparency and accountability, financial institutions can build trust with their customers while effectively managing data privacy and security risks.Share

Bias and Fairness: AI algorithms may reinforce existing biases if trained on biased datasets. It is essential to ensure that AI systems operate fairly and do not discriminate against specific groups. To address these concerns, organizations must prioritize the use of diverse and representative datasets during the training process. Additionally, implementing continuous monitoring and auditing of AI systems can help identify and mitigate bias, ensuring that AI technologies promote equity and inclusivity in decision-making.

Explainability and Transparency: Understanding how certain AI algorithms make decisions can be challenging, particularly in regulated fields like banking and insurance. Financial institutions must strive for transparency and explainability in their AI systems. s. Furthermore, incorporating explainable AI techniques can facilitate compliance with regulatory requirements, ensuring that institutions can effectively justify their algorithms’ outcomes.Share

Regulatory Uncertainty: The regulatory framework for AI is still developing, creating uncertainty for financial institutions. Clearer regulations are necessary to guide responsible AI usage. dditionally, collaboration between regulatory bodies and industry stakeholders can help shape guidelines that ensure innovation while protecting consumer interests. Establishing a standardized framework will not only alleviate uncertainty but also promote best practices in AI deployment across the financial sector.

4. Conclusion

The future of AI in banking and insurance looks promising. As AI technology progresses, we can anticipate the emergence of even more innovative applications. For instance, AI could enable the development of highly personalized financial products, improve the accuracy of market trend predictions, and even establish entirely new financial ecosystems. However, it is essential for financial institutions to tackle the challenges mentioned earlier to ensure responsible and ethical use of AI.

By adopting a proactive and considerate approach, the banking and insurance sectors can leverage AI’s potential to foster a more efficient, secure, and customer-focused financial future. Contact us to get more information about adopting AI.